Plans We Support

We apply our many years of experience to review and recommend which plan structure will be right for our clients. We assess a company’s history, nature of business, management objectives, profitability trends, personnel policies and employee turnover. Additionally, we analyze employee and compensation data to estimate benefits and contributions under various plan formulas.

In the end, a well structured plan will help to attract, retain and motivate employees and help those employees save for their future.

Jump To:

We apply our many years of experience to review and recommend which plan structure will be right for our clients. We assess a company’s history, nature of business, management objectives, profitability trends, personnel policies and employee turnover. Additionally, we analyze employee and compensation data to estimate benefits and contributions under various plan formulas.

In the end, a well structured plan will help to attract, retain and motivate employees and help those employees save for their future.

Jump to:

401(k)

A 401(k) plan is a tax-deferred retirement program that provides substantial tax advantages:

- Employee contributions can be made with pre-tax dollars thus reducing gross taxable income on the employee’s W-2 and possibly increasing take-home pay.

- The earnings from these invested contributions accumulate tax-free while they remain in the plan.

- Taxes are paid only when the money is withdrawn, usually at retirement when employees are typically in a lower tax bracket.

- Can reduce an employee’s current income taxes.

For these reasons and because a 401(k) encourages and often increases employee’s savings, we believe it is the best employee benefit available to employers and their employees today.

Advantages for Employers

Benefits to Employers

- The ability to offer a retirement plan at little expense to the company, which are often concerned about benefit costs.

- Cost-effectiveness—employees fund all or part of the program. In most cases, the employer is not required to make contributions.

- The ability to add a 401(k) plan to an existing benefits package at little cost.

The ability to offer employees a replacement to lost IRA deductions as a result of the Tax Reform Act of 1986. - Company contributions to a 401(k) plan are flexible. The decision to contribute can be made annually.

A 401(k) plan helps attract and retain a skilled and loyal work force, and helps foster good will.

A 401(k) can improve the morale, which can improve productivity and, ultimately, company profits.

Specific Tax Advantages

The IRS has approved the following tax advantages to encourage business owners to establish 401(k) plans.

- Contributions are tax deductible by the employer (IRC § 404).

- Earnings of the trust are tax deferred (IRC § 501).

- Contributions are not subject to federal or state income tax as current income to participants (IRC § 402).

- Benefit distributions at the defined retirement age (and beyond) are tax favored (IRC § 72 and 402).

- IRA rollovers from a 401(k) plan when an participant separates employment are not subject to current taxation.

Advantages for Employees

- A 401(k) plan defers taxes on earnings; employees pay no income tax on the earnings that accumulate until funds are withdrawn.

- Helps employees save through convenient payroll deduction; employees authorize 401(k) contributions to be taken from their salary. They need no discipline to save.

- Increases employee’s take-home pay; employees using a standard saving account will increase their take-home pay because contributions are made on a pre-tax basis.

- Offers employees an alternative to an IRA, with the following added benefits:

- Offers employees a larger deduction: $17,500 or, if age 50 or over, $23,000, for 2014 instead of the $5,500 IRA contribution limit.

- Convenient payroll deductions—employees can avoid the April 15th funding panic that comes with an IRA.

- Greater investment flexibility—employees can choose a pooled investment fund or individual fund selection.

- Greater withdrawal flexibility—employees can make withdrawals at age 55 and upon separation of service without the 10 percent penalty tax for premature withdrawals. An IRA requires the participant to be 59 1/2 to avoid the 10 percent tax upon withdrawal.

- Potential for employer matching contributions—employees can benefit from an employer’s matching contributions, which are not available with an IRA.

Examples of Tax Saving Advantages

Because employee 401(k) contributions are made on a pre-tax basis, the impact on net spendable income is smaller than if the employee was saving the same amount outside the plan.

In addition to these savings under the 401(k) Plan, an employee accumulates a good deal more money because of the tax-free accumulation.

Funding a 401(k) Plan

Employee Pre-Tax Elective Deferrals

The plan can exist with only employee contributions; that is, the company is not required to make any contributions in most cases. The 401(k) can function as a “Super IRA” alternative.

Employee Matching Contributions

Based on the employer’s desire and subject to specific plan design provisions, an employer can match employees’ contributions. Most often, the matching contribution is defined as a percentage of the employee’s contributions. For example, 50% match on each dollar the employee makes up to a 6% employee contribution. However, the match can be any amount and can actually—in more rare cases—exceed the employee contribution. Although the company is not obligated to provide a matching provision in the plan, any level of match will provide a strong incentive for employees to participate.

Discretionary Profit-Sharing Contributions

An employer can incorporate a 401(k) feature into a new or existing profit sharing plan. In addition to determining employee deferrals and matching contributions, the company can determine at the end of each year any additional amounts it wishes to contribute, thereby tying company contributions to its financial performance. When a 401(k) plan is enhanced with profit sharing contributions, the company can increase the total contributions made for the company and its employees.

Qualification Rules and Limits

25 Percent of Compensation Limit

Because a 401(k) plan is considered a profit sharing plan, the maximum deduction that can be taken in any year is 25 percent of total plan compensation. This limit applies to the combined aggregate employee and employer contributions.

$52,000 Limit (IRC § 415)

In any given year, the maximum combined employee and employer contributions that can be made on behalf of an individual employee are subject to a dollar limit of $52,000 a year (in calendar year 2014). An additional $5,000 can be added for employees who are 50 years or older.

$17,500 ($23,000 if age 50 or over) Employee Deferral Limit

The maximum annual employee pre-tax contribution for 2014 is limited to $17,500 per year ($23,000 if over age 50), calculated on a calendar-year basis. The IRS may adjust this figure on an annual basis to reflect the cost of living.

Average Deferral Percentage (ADP) Test

The ADP test is a special non-discriminatory contribution test that is applicable to a 401(k) plan. It assures that contributions made on behalf of highly compensated employees are an acceptable multiple of contributions made on behalf of non-highly compensated employees.

IRA Deduction Rules

Deductible IRA contributions are fully allowed to employees who are not participants in an employer-sponsored 401(k) plan. If an employee is a participant in the 401(k) plan, the tax law restricts the ability to make deductible contributions to an IRA.

The ADP Test

“Average Deferral Percentage” is defined as the average of the ratios calculated separately for each employee of (a) the contributions actually made to the plan on behalf of each employee to (b) the employee’s compensation for the plan year. In general terms and up to prescribed legal limits, the more NHCEs contribute, the more the HCEs can contribute. Therefore, from an employer or business owner’s viewpoint, participation and contribution in the plan by as many employees as possible is critical to the plan’s overall success.

An employee is considered highly compensated if he or she meets any of these criteria:

- Employee is at least a 5 percent owner;

- Employee earned more than $115,000 (as adjusted for inflation) in the prior year.

An employer may elect to limit item 2 above to those who earned more than $115,000 in the prior plan year and were in the top-paid 20 percent of all employees.

Employer matching contributions, along with any employee voluntary contributions, must also all comply with the Average Contribution Percentage (ACP) test, which is similar to the ADP test. Certain multiple-use rules apply when combining the ADP and ACP tests.

401(k) Plan Distributions

Separation from Service

Upon termination of employment, retirement, death or disability.

Termination of the Plan

Upon termination of the plan, the participants become 100 percent vested.

Withdrawals for Hardship

Financial hardship must involve immediate and heavy financial needs that exceed a participant’s reasonably available resources (including a plan loan). The IRS defines financial needs as deductible family medical expenses, the purchase of a principal residence, the next two semesters of college tuition, prevention of eviction, or mortgage foreclosure of a principal residence. All withdrawals are subject to taxation. Additionally, the participant will not be allowed to make contributions for one year following the date of the withdrawal and future contributions will be reduced for the balance of the next calendar year.

Distributions from a plan for a participant younger than 59 1/2 are subject to a 10 percent penalty tax in addition to ordinary income tax. However, there are several exceptions to this penalty tax for distributions made:

- At death or disability

- At early retirement as defined by the plan (after age 55)

- In equal periodic payments (annuity)

- For return of excess 401(k) deferrals

To avoid current taxation, the money may also be rolled over into an IRA. This would continue the tax- sheltered status of the funds until withdrawn.

Participant Loans

Upon termination of employment, before any distribution of the funds is made to a participant, any outstanding loans may be repaid. Any outstanding loan balance not repaid will be deducted from the distribution amount and will be taxable to the participant since loans are not eligible for an IRA rollover.

Vesting

Of course, all employee pre-tax elective deferrals and employee after-tax contributions must always be 100 percent vested, since it was their money to begin with. However, there are various alternative vesting schedules for employer-made contributions based on the employee’s years of service. If employer contributions are used to satisfy the ADP test, then they must also be 100 percent vested.

Alternative vesting schedules include:

Three-Year Cliff

Zero percent for the first two years of service; 100 percent after three years.

Top-Heavy Vesting

Also called “Six-Year Vesting,” 20 percent after one year of service and 20 percent for each additional year; 100 percent after six years.

Investments

The sponsor of the 401 (k) plan has the ability to decide how much discretion participants will have in how their 401(k) funds will be invested.

Two common approaches are:

Trustee-Directed Option

All contributions and deferrals are deposited into a pooled investment fund. Based upon the market climate, the trustee or investment committee will select and invest in any number of investments. Each participant will then share proportionately in the earnings or losses of the pooled fund.

Participant-Directed Options

This approach requires offering a variety of investment vehicles for the participant to choose from that encompass varying risk characteristics. Each participant can select where contributions and/or deferrals will be invested and has the ability to transfer funds from one investment to another during the year. In participant-directed plans, the plan sponsor or the investment professional they are working with will typically offer a range of 10-20 different mutual funds that represent different investment strategies and associated risk levels. Participants share in the earnings or losses of these accounts based on their own investment decisions. It is important to remember, however, that giving employees these investment choices can increase 401(k) recordkeeping and communication costs.

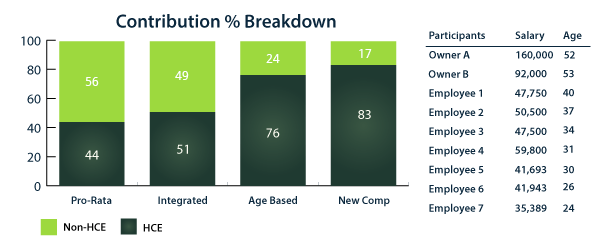

New Comparability

Essentially, this design is attractive to small business owners where they are—as a class or group—typically older than the rank and file employees. The graph below provides a comparison of the percent of the total contribution given to the owners for 4 different plan designs. In this scenario, Owner A and Owner B are considered Highly Compensated Employees (HCE), the remainder of the employees are considered to be non-highly compensated employees (NHCE). Note the larger percentage given to the HCEs in the New Comparability Plan.

The plan design at right is a defined contribution profit sharing plan. Contributions to the plan are made at the employer’s discretion. If business is bad in a given year, the company does not have to make a contribution to the plan as contributions are “discretionary.”

New Comparability

Essentially, this design is attractive to small business owners where they are—as a class or group—typically older than the rank and file employees. The graph below provides a comparison of the percent of the total contribution given to the owners for 4 different plan designs. In this scenario, Owner A and Owner B are considered Highly Compensated Employees (HCE), the remainder of the employees are considered to be non-highly compensated employees (NHCE). Note the larger percentage given to the HCEs in the New Comparability Plan.

Safe Harbor

First, the employer can implement a communication and education campaign to better explain the benefits of participation and contribution to all employees with primary goal of getting more NHCEs to participate and those who are participating to contribute more ea30px3%ch pay period. Alternatively, the employer could modify their plan to include a “Safe Harbor” plan provision.

Beginning January 1, 1999, employers are not required to perform nondiscrimination testing if their plan design meets certain employer contribution requirements called Safe Harbor provisions.

To qualify for this exemption, the employer must make one (but not both) of the following two contributions:

Matching Formula

The employer is required to provide to each non-highly compensated employee a 100 percent match on salary deferrals up to 3 percent of compensation and a 50 percent match on salary deferrals between 3 and 5 percent of compensation. This results in a total match of 4 percent of compensation if the employee contributes 5 percent of their pay into the plan. This contribution must be fully vested (meaning the employee is entitled to 100% of their account balance—including the employer match balance—when they leave the plan).

Non-Elective Contributions

The employer is required to provide non-highly compensated employees a contribution of 3 percent of their compensation. This contribution must also be fully vested.

In this type of plan, the benefits of not having to pay for the added expense of nondiscrimination testing may offset the required employer contributions.